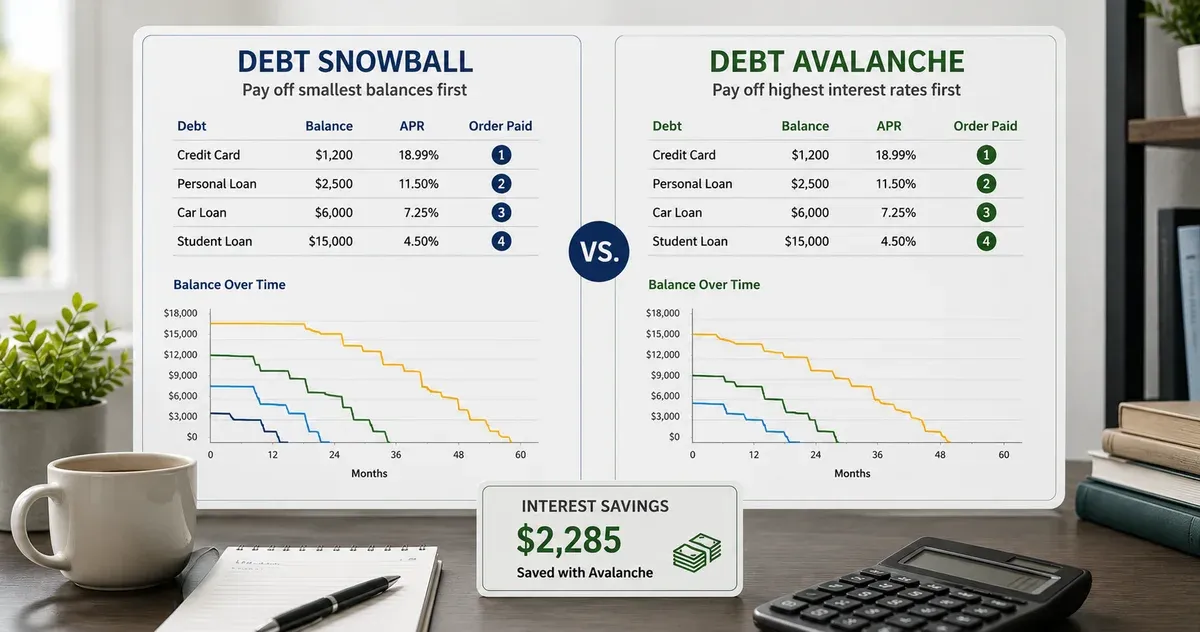

The Debt Avalanche: Mathematically Optimal

The avalanche method directs extra money to the highest-APR debt first, minimizing the total interest paid. It is the mathematically correct approach: interest compounds on the full balance, so eliminating the highest-rate balance fastest reduces the total compounding base as quickly as possible. On a typical household with three debts — a 22% credit card, a 7.5% auto loan, and a 5.8% student loan — the avalanche typically saves $200–$2,000 in interest and 1–6 months compared to the snowball, depending on balances and the extra payment amount available.

The Debt Snowball: Behaviorally Optimal

The snowball method targets the lowest-balance debt first, generating quick "wins" that keep motivation high. Research on behavioral economics — including a 2012 study in the Journal of Marketing Research — found that people are more likely to persist with a debt payoff plan when they see visible progress through early balance eliminations, even if those accounts aren't the most expensive. For someone who has previously abandoned a debt plan, the snowball's psychological structure may produce better real-world outcomes than the mathematically superior avalanche.

The Hybrid Approach

When two debts have similar balances, direct the extra money to the higher APR one — you get the motivational win almost as quickly while saving more on interest. This is especially practical when the highest-APR debt also has a low balance. Sort your debts by APR, then look at the top two or three. If the highest-APR balance is small enough to eliminate within 3 months, treat it as a snowball target. Otherwise, pure avalanche.

The Critical Role of the Extra Payment

Both strategies assume you have a budget that exceeds minimum payments and direct the surplus to the target debt. If you can only afford minimums on all debts, neither strategy can be applied. The most important lever is therefore the size of the extra payment — even $50/month directed to the target debt accelerates payoff significantly. On a $4,500 credit card at 22%, an extra $50/month over the minimum reduces the payoff period by roughly 12 months and saves several hundred dollars.

Consolidation and Refinancing as Accelerators

Debt consolidation loans and balance transfer cards can reduce the interest rate on high-APR debts, making both strategies more effective. A personal loan at 9% consolidating three 20%+ credit cards doesn't eliminate the debt, but it can cut the total interest by 50–60%. Use this calculator before and after a modeled consolidation to quantify the savings. Key caveats: consolidation fees (1–5%), the discipline not to recharge the credit cards after balance transfer, and the risk of turning unsecured debt into secured debt (e.g., home equity loans) where default has more severe consequences.

Building the Payoff Habit

Automated payments are essential for execution. Set the minimum on every debt to auto-pay, then make the extra payment to the target debt as a separate manual or scheduled transfer. This prevents accidental missed minimums (which trigger penalty APRs on credit cards) while keeping the focus on the target. Once the target debt is cleared, roll its entire payment into the next target — that's the "rollover" mechanic that gives both strategies their momentum.

Penalty APRs and Why a Single Missed Payment Costs So Much

Most US credit card agreements include a penalty APR clause that activates after a single payment more than 60 days late, raising the rate to 29.99% on most issuers. Penalty APRs apply to the existing balance and continue for at least six consecutive on-time payments. A single missed payment during a debt payoff can therefore add 8–10 percentage points to your effective interest rate and undo months of progress. This is why the calculator's plan should be paired with automated minimum payments on every debt — even on a snowball plan, every debt other than the target needs its minimum paid on time, every month, with no exceptions. If cash flow is unpredictable, set the auto-pay date 5–7 days before the actual due date to absorb timing risk.

What to Do If a Debt Is in Collections

Debts that have been charged off (typically 180 days delinquent) and sold to a collection agency need different handling than current debts. The original APR no longer accrues; instead the collector tries to negotiate a settlement, often at 30–60% of the face value. Including charged-off debts in this calculator at their face value will overstate your interest cost. The right approach is to enter only currently-accruing debts in the planner and to negotiate charged-off debts separately as lump sums, paid out of the same monthly budget once snowball/avalanche progress frees up cash flow. Always get any settlement agreement in writing before sending payment, and verify after that the debt is reported as "settled" or "paid in full" rather than "settled for less."

How to Pay Off Debt Fast: The 5 Levers That Actually Work

The phrase "pay off debt fast" shows up in millions of search queries every month because people want a concrete, actionable answer — not a vague budgeting pep talk. The five levers below are ordered by impact. Applying even two or three of them together can cut your payoff timeline by 30–50%.

1. Increase the monthly surplus. This is the single largest lever. On a $12,000 debt portfolio at an average 18% APR, raising your monthly payment from $350 to $500 reduces payoff time by roughly 14 months and saves over $1,800 in interest. Use the calculator to model the exact impact: simply raise your budget field and watch the months drop. Even $50–100/month extra makes a measurable difference.

2. Eliminate the highest-APR debt first (avalanche). Directing your surplus to the highest-interest balance first minimizes how much new interest accumulates on the rest of the portfolio. On a typical three-debt household, this saves $300–$1,500 versus paying the smallest balance first. The calculator runs both strategies and shows the exact difference in the comparison table.

3. Make biweekly payments instead of monthly. If you split your monthly payment in half and pay every two weeks, you end up making 26 half-payments per year — equivalent to 13 monthly payments instead of 12. That one extra payment per year reduces principal faster and cuts compounding. On a $8,000 credit card at 22% APR, biweekly payments save roughly $400 and shave 4–5 months off the payoff versus monthly payments of the same total amount.

4. Apply windfalls directly to the target debt. Tax refunds, bonuses, and unexpected income are the highest-return debt payments you can make — because they reduce principal immediately, which reduces all future interest on that balance. A $1,500 tax refund applied to a 22% APR card eliminates $330/year in recurring interest from that point forward. Rule of thumb: allocate at least 70% of any windfall to the current target debt; keep 30% as a buffer to avoid a short-term cash crunch that forces you to carry more credit card charges.

5. Negotiate or refinance high-rate debt. Calling your credit card issuer and requesting a lower APR succeeds roughly 25% of the time for customers with a strong payment history. A reduction from 24% to 18% on a $6,000 balance saves ~$360/year in interest — without changing your payment amount. Similarly, a personal loan consolidation at 10% replacing three 20%+ credit cards can cut total interest by 40–50%. Use the calculator to model the consolidated scenario: enter the new loan as a single row with the consolidated balance and lower APR, and compare the payoff timeline against the multi-card status quo.

How to Optimize Your Debt Payoff Strategy

Optimization means choosing the combination of strategy, payment size, and timing that minimizes total interest paid while staying executable given your real cash flow. Here is the practical framework:

Step 1 — List all debts. Enter every account: balance, APR, and minimum. Include medical bills, personal loans, car loans, and any 0% promotional balances (0% is still worth including to track their payoff timing and the post-promo APR risk).

Step 2 — Find your true surplus. Add up all minimums; subtract from your monthly income after fixed expenses. The remainder is your maximum sustainable budget. Set the calculator budget to 80–90% of that maximum — leave a small buffer to avoid undershooting due to irregular expenses.

Step 3 — Run both strategies and compare. The comparison table shows months and interest for snowball vs avalanche. If the interest difference is under $500, the choice is mostly psychological; if it's over $1,000, avalanche is worth the behavioral discipline. Choose the strategy you will actually sustain.

Step 4 — Review every quarter. Re-run the calculator after any income or expense change larger than 5%. After a raise, raise the budget field first — every additional dollar compounds faster than anything else.

Step 5 — Automate minimums, manual the extra. Set every minimum to auto-pay to avoid penalty APRs. Make the extra payment manually to the target debt each month — the deliberate act reinforces the goal. Once the target debt is cleared, roll its full payment into the next target immediately (this is the "rollover" that gives both strategies their accelerating power).

How to Re-Plan When Your Income Changes

A debt payoff plan is rarely linear over its full term. Annual raises, bonuses, tax refunds, and side income all create opportunities to accelerate; medical events, layoffs, and major repairs force temporary slowdowns. The discipline is to re-run the calculator at least once per quarter, plus immediately after any income shift larger than 5%. After a raise, allocate at least half of the new take-home to the current target debt — this is the easiest moment to accelerate because the increase hasn't yet been absorbed by lifestyle. After an income drop, drop your monthly extra to whatever still leaves room for essential savings and a small emergency buffer; restoring it once your income recovers is psychologically easier than restarting from scratch after the plan collapses.

Including Mortgages and Student Loans in the Plan

Whether to include long-term, low-rate debts like mortgages and federal student loans in a snowball/avalanche plan depends on the gap between their APR and your realistic risk-free return on cash. A 30-year mortgage at 4% behaves very differently from a 22% credit card: in a high-interest savings or T-bill environment yielding 4–5%, paying extra principal on the mortgage produces a guaranteed return below what idle cash already earns, so accelerating it is mathematically neutral or slightly negative before tax considerations. Federal student loans complicate the picture further because of income-driven repayment plans, public service forgiveness eligibility, and interest subsidies on subsidized loans during certain status periods — accelerating payment can forfeit benefits that are worth more than the interest saved. The pragmatic rule for the calculator: include any debt with an APR above your safe cash yield plus 2 percentage points; exclude debts below that threshold and treat their minimums as fixed expenses. Re-evaluate annually, since both your APRs and the prevailing risk-free rate shift over time. For someone whose only high-rate debts are credit cards and an auto loan, the snowball/avalanche plan should usually run on those alone, with the mortgage and federal student loans paid only at minimum until everything above the threshold is cleared.