When paying off multiple debts simultaneously — credit cards, personal loans, medical bills, student loans — the order in which you eliminate them has a significant impact on total interest paid and time to debt freedom. Two dominant strategies have emerged from personal finance practice: the debt snowball, which prioritizes the smallest balance, and the debt avalanche, which prioritizes the highest interest rate. This article explains both with exact math, examines the behavioral factors, and provides a framework for choosing the right approach for your specific situation.

The Debt Avalanche: Maximum Mathematical Efficiency

The avalanche method directs any surplus payment (money available above all minimum payments) to the debt with the highest APR. Once that debt is eliminated, the total payment freed up — both the minimum and the extra — is redirected to the next-highest-APR debt. The name "avalanche" reflects the accelerating effect as each eliminated debt adds to the payment directed at the next one.

Why it minimizes interest: Every dollar of principal carries an ongoing interest charge equal to the balance multiplied by the monthly rate. Eliminating high-rate principal first removes the most expensive interest generation. Mathematically, the avalanche is always the optimal ordering when minimizing total interest paid is the only objective.

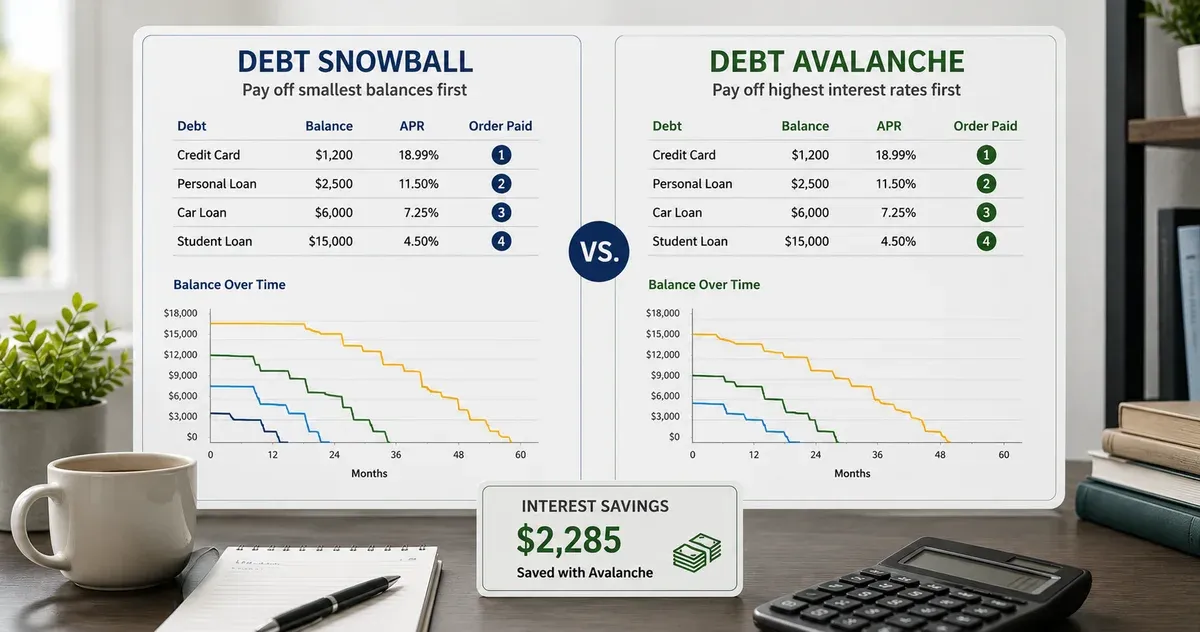

Example — three debts, $500/month available over minimums:

- Debt A: $8,000 balance, 22% APR, $200 minimum

- Debt B: $3,500 balance, 15% APR, $100 minimum

- Debt C: $5,000 balance, 8% APR, $120 minimum

Total minimums: $420. Extra payment applied to Debt A (highest APR): $80/month. Avalanche result: ~42 months to debt freedom, ~$5,200 total interest.

The Debt Snowball: Behavioral Traction

The snowball method directs surplus payments to the debt with the smallest current balance, regardless of APR. The premise is psychological: eliminating a debt account creates a sense of accomplishment and tangible progress that reinforces the behavior and sustains motivation over a multi-year payoff period.

Why it sometimes outperforms theoretically: The mathematical difference between snowball and avalanche is often smaller than intuition suggests — especially when the high-APR debts also happen to be the largest balances. And if a theoretically superior strategy is abandoned halfway through because of motivational collapse, it produces worse outcomes than a slightly suboptimal strategy that gets completed. Research by Amar Cheema and Dilip Soman (2008) and by David Gal and Blakeley McShane (2012) found that progress metrics based on number of debts eliminated (not balance reduction) were stronger predictors of payoff completion.

Using the same three debts, snowball prioritizes Debt B ($3,500) first, then Debt C ($5,000), then Debt A ($8,000). Snowball result: ~44 months to debt freedom, ~$5,900 total interest. The snowball costs about $700 more in this scenario — but eliminates one account 12–18 months earlier, providing a motivational win that can matter.

Head-to-Head Comparison: When Does the Gap Matter?

The financial difference between snowball and avalanche varies by scenario. The gap is largest when:

- The highest-APR debts are also the largest balances (avalanche attack is both high-rate and high-balance)

- The APR spread is large (e.g., a 25% card vs. a 7% loan)

- The payoff timeline is long (more months for the interest difference to compound)

The gap is smallest when:

- Balances and rates are similar across debts

- The highest-rate debts also happen to be the smallest balances (then snowball and avalanche pick the same target)

- The timeline is short (less time for compounding to diverge)

Use the Debt Payoff Calculator to input your actual debts and see the exact dollar and month difference for your specific situation. The comparison tab shows both strategies side by side with full payoff timelines.

How to Choose

Choose the avalanche if:

- You have a high-APR debt that is also a large balance (e.g., $12,000 at 24%) — the savings are substantial

- You have a strong track record of sustaining financial plans without external motivation reinforcement

- The APR spread across your debts is large (15%+ difference between high and low rate)

- You are mathematically motivated and the interest savings number feels tangible and motivating

Choose the snowball if:

- You have several small-balance debts (under $1,500) that can be eliminated in 3–6 months — providing early wins

- You've started debt payoff plans before and abandoned them — behavioral re-engagement is the primary obstacle

- The APR spread is small (under 5%) — the financial cost of snowball is negligible

- Monthly complexity of managing many accounts is creating friction

Hybrid approach: Start with snowball to eliminate 1–2 small accounts and build momentum, then switch to avalanche for the remaining larger balances. This hybrid is not theoretically optimal but may be the most effective in practice for people who need early wins to sustain the longer payoff journey.

The Monthly Surplus: The Most Important Variable

The choice between snowball and avalanche is meaningful, but the size of the monthly surplus directed toward payoff is far more impactful. The difference between a $200/month surplus and a $350/month surplus — applied to the same three-debt portfolio — is typically 12–18 months of payoff time and $1,500–$2,500 in interest, regardless of ordering strategy.

Before optimizing the payoff order, maximize the surplus by:

- Canceling underused subscriptions

- Redirecting any seasonal or irregular income (bonus, tax refund, side income)

- Temporarily reducing retirement contributions above the employer match

- Reviewing insurance rates annually

The Debt Payoff Calculator's "What If" slider lets you see how each $50 increase in monthly surplus shortens the timeline and reduces total interest — often the most powerful insight the tool generates.

Tracking Progress During Payoff

Multi-year debt payoff plans benefit from a structured progress tracking mechanism. Specific practices that help:

- Monthly balance updates: Log each debt balance monthly. Watching the trajectory decline creates the same psychological feedback as the account eliminations in the snowball.

- Interest saved running total: Track cumulative interest paid vs. what you would have paid on minimums only. This "interest avoided" metric reinforces the value of staying on plan.

- Projected payoff date: Recalculate after each payment — if you're ahead of schedule, the updated payoff date is motivating. If behind, it triggers a corrective discussion.

The Debt Payoff Calculator generates a month-by-month payoff table for all debts across the selected strategy, which can serve as the source for a progress tracking spreadsheet.

Hybrid Strategies and When Pure Avalanche Loses

The two named methods get the attention, but in practice many people execute a hybrid that performs better than either pure approach. The most useful variant is the blended snowball: sort debts by APR, then identify the top two or three. If any of those highest-APR debts also has a small balance — small enough to pay off within 2–3 months at your available extra payment — attack it first. You get an early elimination win (the snowball's behavioral payoff) on the same debt that the avalanche would prioritize anyway. Only after that quick win do you continue down the avalanche order.

A second hybrid is tier-locking. Group debts into two or three tiers by APR — say, anything above 20% in the top tier, 10–20% in the middle, and below 10% in the bottom. Within each tier, use snowball ordering (smallest balance first) for motivation. Between tiers, work top-to-bottom regardless of balance. This produces 80% of the avalanche's interest savings with most of the snowball's behavioral pull, and it's much easier to explain to a partner who doesn't want a spreadsheet conversation every month.

Pure avalanche genuinely loses in two scenarios. First, when the highest-APR debt is also the largest balance and would take 18+ months to eliminate without any visible progress milestones, the dropout risk often exceeds the interest savings. Second, when you have a single small debt under $500 that's been hanging around for years — a forgotten medical bill, an old retail card — paying it off as a one-time clear-the-deck move, even out of avalanche order, often unlocks a psychological reset that the avalanche numbers don't capture.

Common Mistakes That Sabotage Both Strategies

Five mistakes show up repeatedly in failed payoff plans, regardless of which method was chosen. Recognizing them in advance is the cheapest form of insurance against another year of progress lost.

Skipping the budget step. Both methods assume a known monthly surplus directed at the target debt. Without an actual budget — even a rough one — the surplus is theoretical, and the extra payment becomes whatever happens to be in the checking account on the due date. Build the budget first; the strategy choice matters far less than the consistency of the extra payment.

Closing accounts after payoff. Closing a credit card after paying it off feels like closure, but it shortens credit history length and can spike utilization on remaining cards — both of which damage credit scores at exactly the moment you might want to refinance other debts at lower rates. Leave the account open with a $0 balance and consider a small recurring auto-pay (a streaming subscription) so the issuer doesn't close it for inactivity.

Borrowing from retirement to pay debt. 401(k) loans and early withdrawals to clear consumer debt feel mathematically attractive when retirement returns are uncertain and credit card APRs are 20%+. The hidden costs — lost compounding, double taxation on the loan repayment, the ten-percent penalty on early withdrawals — typically erase the headline savings. Treat retirement balances as off-limits except in narrowly defined emergency scenarios.

Ignoring the minimum on non-target debts. Both strategies require paying minimums on every debt, with the extra going only to the target. Missing a minimum on a non-target debt because all spare cash went to the target triggers late fees and — critically — may activate a penalty APR that wipes out months of interest savings. Automate the minimums; manage the extra payment manually.

Treating the plan as binary. Plans get abandoned when the language shifts from "I am paying down debt" to "I have failed at paying down debt." A month at half the planned extra payment is still progress. A month skipped entirely is a setback, not a failure. Resilient plans treat slow months as part of the plan, not as exits from it.