"How much car can I afford?" is the wrong question if you only look at the sticker price or the monthly payment a dealer quotes. Affordability is a relationship between three numbers: how much you put down, how long you borrow, and how large the total cost of driving is relative to your income. The 20/4/10 rule is a widely cited rule of thumb that ties all three together into one simple test. This guide explains what the rule means, walks through the payment-to-income math, shows why long loan terms create negative equity, and demonstrates how your down payment changes what you can responsibly buy. It pairs directly with the Car Loan Calculator, which lets you plug in your own numbers and test the rule in seconds.

What the 20/4/10 Rule Actually Says

The 20/4/10 rule is a guideline, not a law or a lender requirement. It is promoted by major banks and auto-finance educators as a quick sanity check before you sign. It has three parts:

- 20 — Put at least 20% down. A down payment of one fifth of the purchase price reduces the amount you finance and, critically, gives you equity from day one.

- 4 — Finance for no more than four years (48 months). A shorter term means you pay less interest overall and pay the loan down fast enough to stay ahead of depreciation.

- 10 — Keep total transportation costs at or below 10% of your gross monthly income. As Chase and other lenders describe it, the 10% is based on gross (pre-tax) income, and "total transportation costs" means the loan payment plus insurance, fuel, and maintenance — not the payment alone.

That last point is where most buyers get it wrong. They compare only the monthly payment to their budget and forget that insurance, gas, and upkeep can add hundreds of dollars a month. The 20/4/10 rule forces you to budget for the whole cost of driving.

The 10% Test: Payment-to-Income Math

Start with your gross monthly income — your pay before taxes and deductions. Multiply by 10% (divide by 10). That figure is your entire monthly transportation budget. Then subtract your other car costs to find how much is left for the loan payment itself.

Consider a household earning $80,000 per year, which is about $6,667 gross per month:

- 10% of gross monthly income: $667 — the total transportation budget

- Estimated insurance: $160/month

- Estimated fuel: $130/month

- Estimated maintenance and repairs: $60/month

- Remaining for the car payment: $667 − $350 = $317/month

A $317 monthly payment at a 7% APR over 48 months finances roughly $13,300 in principal. Add the required 20% down payment, and this household is looking at a total vehicle price of about $16,500. That may feel low against today's average transaction prices — and that is exactly the point of the rule. It reveals the gap between what dealers will approve you for and what actually fits your budget without crowding out savings, rent, and everything else.

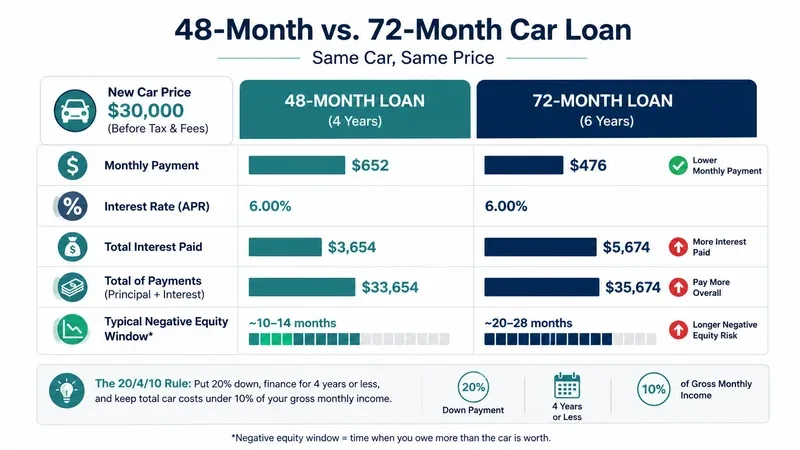

The 4-Year Term: Why Long Loans Backfire

Stretching a loan term lowers the monthly payment, which is why 72- and 84-month auto loans have become common. But a longer term increases total interest and — more dangerously — keeps you "underwater" for years. Take the same car financed at 7% APR:

- 48-month term: about $718/month on a $30,000 loan, roughly $4,500 total interest

- 72-month term: about $512/month on the same $30,000 loan, roughly $6,800 total interest

The 72-month loan saves about $206 a month but costs roughly $2,300 more in interest — and it takes far longer to build equity. This is not just a math problem; it is a documented consumer risk. The Consumer Financial Protection Bureau warns that "a longer loan puts you at risk for negative equity over a longer period of time," where negative equity means you owe more on the vehicle than it is worth.

Why Long Terms Cause Negative Equity

A new vehicle loses value quickly — commonly around 20% in the first year alone. On a short loan with a solid down payment, your balance falls faster than the car depreciates, so you keep positive equity. On a long, low-down-payment loan, the balance falls slowly while the car keeps depreciating, so for a stretch of the loan you owe more than the car is worth.

The CFPB's analysis of auto-finance data found that negative equity is widespread and rising: across loans originated between 2018 and 2022, roughly 11.6% of vehicle loans included negative equity rolled in from a prior trade-in, peaking at over 17% in 2020. The Bureau also reported that by late 2023, about one in five vehicles traded in carried negative equity. Most importantly, the CFPB found that consumers who financed negative equity were more than twice as likely to have their loan sent to repossession within two years compared with buyers who traded in a car with positive equity.

The 4 in 20/4/10 exists to keep you out of this trap. A 48-month payoff on a car with 20% down keeps your equity positive through almost the entire loan, so you can sell or trade without writing a check to cover the shortfall. If you later end up rolling an old balance into a new loan, model it first with the trade-in and negative-equity guide so you can see the real cost before signing.

How the Down Payment Changes Affordability

The 20% down payment does more than shrink the monthly payment — it changes your entire equity position and your risk exposure. Compare a $35,000 car financed at 7% APR over 48 months:

- 0% down (finance $35,000): about $838/month, roughly $5,200 total interest, and you are underwater from the moment you drive off the lot.

- 20% down ($7,000, finance $28,000): about $670/month, roughly $4,200 total interest, and you start with meaningful equity that cushions against depreciation.

The 20% down payment cuts the monthly cost by roughly $168, saves about $1,000 in interest, and — the part that never shows up on the dealer's worksheet — protects you if the car is totaled early. Insurance pays the car's market value, not your loan balance, so a small down payment on a long loan can leave you owing money on a car you no longer have. GAP insurance covers that gap but adds cost; a healthy down payment reduces the need for it.

If you cannot reach 20% down on the car you want, the honest conclusion is usually that the car is too expensive for your situation right now, not that the rule is wrong. Buying a less expensive vehicle to hit 20% down is almost always cheaper than adding GAP insurance and stretching the term on a pricier one.

When the 20/4/10 Rule Is Hard to Meet

The rule was calibrated for a car market with lower prices than today's. With average new- and used-car prices well above where they sat a decade ago, and financing rates for new-car loans hovering in the high-6% to 7% range in 2026 according to the Federal Reserve's G.19 data and lender rate surveys, many buyers find the 10% ceiling difficult to hit. Some financial commentators now suggest a more realistic target of roughly 12% to 15% of gross income for total transportation costs when the strict 10% is out of reach.

Treat that as a flex, not a free pass. Every percentage point you add to the transportation share is a percentage point that cannot go toward rent, retirement, or an emergency fund. If you must go above 10%, keep the 20% down and the four-year term intact — those two guardrails are what protect you from negative equity and repossession risk. The income share is the part that flexes; the down payment and term are the parts that keep you safe.

Putting the Rule to Work With the Calculator

The fastest way to apply the 20/4/10 rule to a specific car is to test it directly. In the Car Loan Calculator, enter the vehicle price, set the down payment to 20% of that price, set the term to 48 months, and enter a realistic APR for your credit tier. The calculator returns the monthly payment, total interest, and full amortization schedule. Then check the payment against your 10% transportation budget after subtracting insurance, fuel, and maintenance. If the payment fits, the car passes the rule. If it does not, you have three levers: a bigger down payment, a cheaper car, or — as a last resort — a longer term, with the negative-equity cost that comes with it.

For the mechanics of how APR, term, and down payment interact on any auto loan, see the companion car loan guide. Used together, the guide, this rule, and the calculator turn "how much car can I afford?" from a gut feeling into a number you can defend.