Buying a car is one of the largest financial decisions most households make — typically the second most expensive purchase after a home. Yet many buyers focus almost exclusively on the monthly payment, often without understanding how that payment translates to total cost. A $450/month payment on a 72-month loan can represent $5,000–$8,000 more in total spending than a $550/month payment on a 48-month loan for the same vehicle. This guide explains how APR, loan term, down payment, trade-in value, and taxes interact to determine the true cost of financing a car.

How Car Loan Interest Works

Auto loans use simple interest amortization. Each monthly payment consists of an interest component and a principal component. The interest for any given month equals the remaining balance multiplied by the monthly rate (APR/12). As the balance decreases, the interest component shrinks and the principal component grows — this is an amortizing loan.

The key formula is the standard loan payment formula:

PMT = P × [r(1+r)^n] / [(1+r)^n − 1]

Where P is the principal (amount financed), r is the monthly rate (APR/12), and n is the number of payments. The Car Loan Calculator solves this instantly for any combination of inputs and shows the full amortization schedule.

APR: The True Cost of Borrowing

APR (Annual Percentage Rate) is the annualized cost of borrowing. Unlike the interest rate on its own, APR includes fees (though for most auto loans, the nominal rate and APR are identical). Even small APR differences have a significant impact on total cost:

- $25,000 financed at 5% APR for 60 months: $472/month, $3,307 total interest

- $25,000 financed at 7% APR for 60 months: $495/month, $4,702 total interest

- $25,000 financed at 9% APR for 60 months: $519/month, $6,125 total interest

The difference between a 5% and 9% APR on a typical car loan is about $2,800 in total interest — roughly the cost of an extended warranty or a major maintenance event. APR is determined by your credit score, loan term, lender, and whether you're buying new or used. New car rates are generally 1–2 points lower than used car rates. Credit union rates are typically 1–2 points lower than dealership financing.

Practical tip: Get pre-approved by your bank or credit union before visiting the dealership. This gives you a fallback rate and negotiating leverage against dealer financing.

Loan Term: Monthly vs. Total Cost Trade-off

Extending the loan term lowers monthly payments but significantly increases total interest paid. Many buyers optimize for the lowest monthly payment, inadvertently choosing terms that maximize lender revenue.

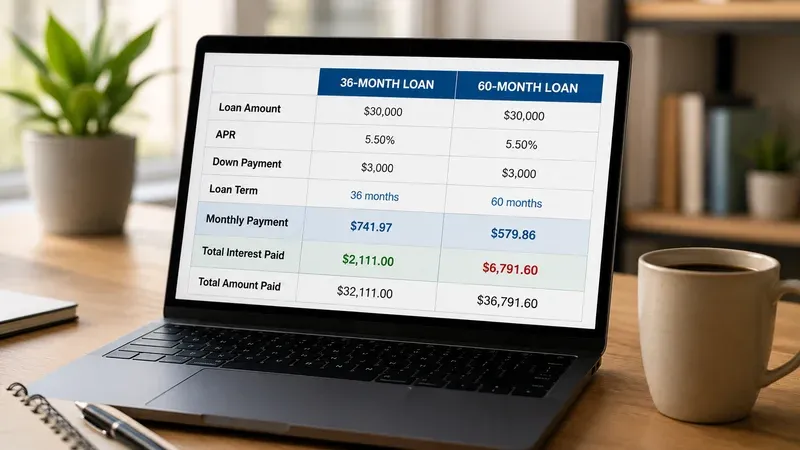

$30,000 at 6.5% APR across four terms:

- 36 months: $920/month | $3,101 total interest

- 48 months: $712/month | $4,150 total interest

- 60 months: $587/month | $5,219 total interest

- 72 months: $505/month | $6,309 total interest

The 72-month loan costs $3,209 more in interest than the 36-month loan. Worse, longer-term loans create underwater risk — the loan balance can exceed the car's depreciated market value for an extended period, leaving you unable to sell or trade without paying the difference out of pocket.

A widely-used rule of thumb: for new cars, choose a term of 48–60 months maximum; for used cars, 36–48 months to align the loan payoff with reasonable remaining vehicle life.

Down Payment: How It Affects More Than Just the Monthly Amount

A larger down payment reduces the amount financed and thus the monthly payment and total interest. But it also affects your equity position from day one, reducing underwater risk. Cars typically depreciate 20–30% in the first year; without a sufficient down payment, you can quickly owe more than the car is worth.

A standard recommendation is 20% down on a new car and 10% on a used car. On a $35,000 new vehicle, 20% down ($7,000) reduces the financed amount from $35,000 to $28,000 at 6% APR for 60 months:

- 0% down: $677/month, $5,619 total interest, high underwater risk year 1–2

- 20% down: $541/month, $4,494 total interest, minimal underwater risk

The down payment also reduces risk of being "upside down" if the car is totaled — insurance pays market value, not loan balance. GAP insurance mitigates this risk but adds to total cost.

Trade-In Value and Tax Benefits

When you trade in a vehicle, the dealer applies the trade-in value as a credit toward the purchase price. In most US states, this reduces the taxable purchase amount — meaning you pay sales tax only on the difference between the new vehicle price and the trade-in value, not the full purchase price.

Example: You buy a $32,000 car and trade in a vehicle worth $8,000 in a state with 8% sales tax:

- Without trade-in tax benefit: Sales tax = $32,000 × 8% = $2,560

- With trade-in tax benefit: Sales tax = ($32,000 − $8,000) × 8% = $1,920

- Tax savings: $640

The Car Loan Calculator applies this trade-in tax benefit automatically when computing the total financed amount. Note that not all states offer this tax benefit (e.g., California does not reduce the taxable basis for trade-ins). Confirm your state's rules before finalizing the calculation.

Total Cost of Ownership vs. Total Loan Cost

The car loan cost is only part of the ownership picture. Comparing loans accurately requires including:

- Insurance: New cars, longer loan terms, and gap insurance all increase premiums

- Registration and taxes: Annual costs that vary by state and vehicle value

- Maintenance and repairs: Used cars typically have higher maintenance costs but lower loan costs

- Fuel: Fuel efficiency differences between vehicles create real annual cost differences

- Depreciation: The largest single cost component for most vehicle purchases

The Car Loan Calculator focuses on financing cost — the computable, math-driven component. Use it alongside your insurance quotes and maintenance estimates to build a full picture before committing.

How to Use the Car Loan Calculator

The Car Loan Calculator takes vehicle price, down payment, trade-in value, sales tax rate, APR, and loan term as inputs and returns:

- Monthly payment

- Total financed amount (after down payment, trade-in, and taxes)

- Total interest paid over the loan life

- Total loan cost (principal + interest)

- Full amortization schedule showing balance, payment, interest, and principal for each month

The term comparison tool shows two loan terms side by side, making the monthly vs. total cost trade-off immediately visible. The rate comparison tool does the same for different APRs — useful when comparing dealer financing against a credit union pre-approval.

Refinancing an Auto Loan: When It Makes Sense

Most buyers treat the auto loan as fixed once signed, but refinancing is a legitimate lever to cut total cost — especially if your credit profile improved after purchase, or if market rates dropped. Many credit unions and online lenders refinance auto loans with no origination fee once the original loan has seasoned for 60–90 days. The mechanics are simple: a new lender pays off the old loan and issues a new loan at a different rate, term, or both.

The decision rule has three components. First, the rate gap: refinancing usually only makes sense if the new APR is at least 1 percentage point lower than the current one. Second, the remaining term: refinancing late in the original loan (less than 12–18 months left) rarely produces meaningful savings because most of the interest is already paid — auto loans amortize like mortgages, with interest-heavy early payments. Third, the cost of any title fees, registration changes, or prepayment penalties on the original loan; some loans have a precomputed interest structure that makes early payoff less rewarding than the remaining balance suggests.

A practical example: on a 60-month, $30,000 loan originally at 9.5% APR, refinancing after 12 months to 6.5% APR with 48 months remaining saves roughly $1,700 in remaining interest. The same refinance attempted with only 18 months left would save closer to $400 — worth doing, but a much smaller payoff for the paperwork involved. Run the numbers in the calculator twice: once for the remaining schedule of the original loan, and once for the new schedule with the proposed refinance terms. The difference in remaining total interest is the actual savings.

One trap to avoid: refinancing into a longer term to drop the monthly payment. This often turns a refinance from a savings move into a more expensive one, even at a lower APR, because you stretch the principal over more months. If cash flow is the goal, the term extension may still be defensible, but be honest about whether you're saving money or just rearranging when you pay it.

GAP Insurance, Extended Warranties, and Dealer Add-Ons

The financing desk at a dealership is structured as a profit center, not a service. The car is sold; the F&I (finance and insurance) phase is where margin is recovered through add-on products. The most common add-ons are GAP insurance, extended warranties, paint and fabric protection, key replacement plans, and tire-and-wheel coverage. Some have genuine value; many are priced 2–3x what equivalent coverage costs from a third party.

GAP insurance covers the difference between your loan balance and the actual cash value of the car if it's totaled or stolen. It's most relevant when you put little down on a long-term loan, because vehicles depreciate faster than the loan amortizes during the first 1–2 years — you can owe more than the insurance payout. GAP from a dealer typically costs $400–$1,000 financed into the loan; equivalent GAP from your auto insurer or credit union usually costs $20–$50/year, billed separately. The dealer version is convenient but often 5–10x more expensive over the loan term, and financing it means paying interest on the GAP cost itself.

Extended warranties (technically vehicle service contracts) are similar. The price markup is significant, exclusions are dense, and the claim process often requires authorized repair facilities. For a vehicle still under factory warranty for 3–5 years, an extended warranty bought at the time of purchase can be re-evaluated later — most providers will sell coverage at any time before the factory warranty expires, often at lower cost when bought from a third party rather than the dealer.

The pragmatic rule: never decide on add-ons during the F&I conversation. Ask for the specific terms in writing, take them home, and compare against third-party providers and your existing insurance. Anything that requires a same-day decision is almost always overpriced. If a dealer insists, walk away from that specific add-on; the financing terms themselves can almost always still be accepted without the bundle.

When running this calculator, model the price of any add-on as if it were a separate line item rather than rolling it silently into the loan. Adding $1,200 of GAP and warranty to a $30,000, 60-month, 7% loan adds about $24/month in payments and roughly $230 in interest — a hidden cost that doesn't appear in the headline monthly payment number you negotiated.