Most savings advice is aspirational but not operational. "Save more" is not a plan — a plan specifies a target amount, a deadline, a monthly contribution, and an expected interest rate. Without those four inputs, there is no feedback loop, no progress signal, and usually no sustained behavior. This guide shows you how to construct a savings plan with the same precision a financial planner would apply, using basic math and a savings goal calculator to make every trade-off visible.

Step 1: Define the Goal Precisely

Vague goals — "I want to save more" or "I want an emergency fund" — fail because they don't generate a concrete target. Precise goals do: "I want $10,000 in an emergency fund within 24 months" or "I want $25,000 for a house down payment by July 2027."

For each goal, specify:

- The target amount: Research the actual cost. An emergency fund is typically 3–6 months of essential expenses. A down payment is typically 10–20% of a home purchase price plus closing costs.

- The deadline: A specific date creates urgency and allows you to calculate the required contribution rate.

- The interest rate: High-yield savings accounts in 2024–2025 are offering 4.5–5.0% APY. This matters — on a 3-year savings plan, interest can cover 5–10% of your target, meaningfully reducing required contributions.

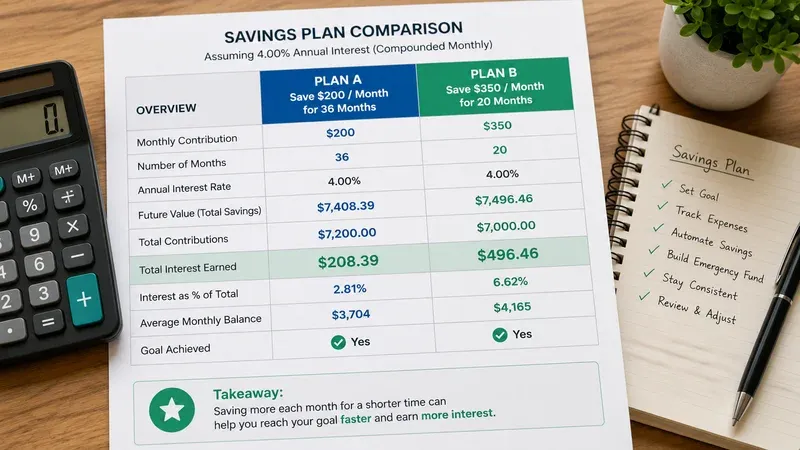

Step 2: Calculate the Required Monthly Contribution

The math behind a savings goal is a standard future value of annuity formula. If you make a monthly contribution C to an account earning monthly rate r = APY/12 for n months, the accumulated balance is:

FV = C × [(1+r)^n - 1] / r

Solving for C (what you need to save per month to hit the target) is what the Savings Goal Calculator does instantly. But understanding the inputs helps you make smarter adjustments.

Example: You want $15,000 in 30 months with a 4.8% APY account.

- Monthly rate r = 0.048/12 = 0.004

- Future value needed = $15,000

- Required monthly contribution ≈ $472

If $472/month is more than your budget allows, the Savings Goal Calculator shows you two options: reduce the target, extend the timeline, or both. You can also flip the calculation — enter a fixed monthly contribution and see how long it takes to reach the goal.

Step 3: Prioritize Multiple Goals

Most people are saving for more than one thing simultaneously — an emergency fund, a vacation, a car, retirement. Prioritizing incorrectly creates the illusion of progress while actually spreading money too thin to reach any goal efficiently.

A practical priority framework:

- Employer 401(k) match first: This is an instant 50–100% return on contributions. Never leave it on the table.

- Emergency fund: Without 3–6 months of expenses in liquid savings, any financial shock — job loss, medical bill, car repair — forces you to take on high-interest debt. Build this before other goals.

- High-interest debt payoff: Debt at 18%+ APR is more urgent than saving at 5% APY. See our Credit Card Payoff Calculator.

- Medium-term goals: Down payment, car, wedding, travel fund.

- Long-term investing: IRA, taxable brokerage, education savings.

Step 4: Automate Contributions on Payday

The single most effective change most people can make to their savings behavior is automating contributions so the money moves to savings before discretionary spending decisions happen. This is the "pay yourself first" strategy — and it works because it removes the willpower requirement entirely.

Set up an automatic transfer from your checking account to a high-yield savings account on the same day your paycheck deposits. Start with a fixed dollar amount (not a percentage, which requires recalculation when income varies). Even $100/month automated beats $300/month manually — because the $300 manual contribution often becomes $150 or zero when competing expenses arise.

Step 5: Account for Interest — It Changes the Math

In a zero-interest environment, a $12,000 goal over 24 months requires exactly $500/month. At 5% APY, the required contribution drops to about $476/month — saving you roughly $565 in contributions over the period. At higher amounts and longer timelines, this compounding effect is dramatically larger.

For a 5-year savings goal of $60,000 at 5% APY, the required monthly contribution is approximately $882. Without interest (0% APY), you'd need $1,000/month — a difference of $118/month or about $7,060 over 5 years. This is why choosing a high-yield account over a standard savings account (which in 2024 averages 0.46% APY nationally) matters significantly.

Step 6: Review and Adjust Quarterly

Savings plans degrade when life changes outpace plan updates. A quarterly review — 15 minutes, once every 3 months — keeps the plan current and maintains the feedback loop:

- Check current balance vs. expected balance at this point in the plan

- If behind: identify the reason (emergency withdrawal, contribution shortfall) and recalculate the new required monthly amount

- If ahead: either accelerate the deadline or increase the target

- Check the interest rate on your account — if rates have moved significantly, update the calculation

Common Savings Plan Mistakes

- Setting a target without a deadline: Creates no urgency and no calculable contribution requirement.

- Saving what's "left over" each month: Discretionary spending consistently absorbs leftover income. Pay yourself first.

- Keeping savings in a 0.5% APY account: Leaving $20,000 in a traditional savings account instead of a 5% HYSA costs you roughly $900/year in foregone interest.

- Conflating savings and investment: Emergency funds and near-term goals (under 3 years) belong in FDIC-insured savings accounts. Investment accounts for longer-term goals offer higher expected returns but with volatility that can create a shortfall when you need the money.

- Not accounting for inflation: For goals 5+ years out, factor in inflation. Use the Inflation Calculator to estimate what a nominal savings target will actually buy in the future.

How the Savings Goal Calculator Helps

The Savings Goal Calculator supports two modes that mirror the two most common savings planning questions:

- How much do I need to save per month? Enter the target amount, timeline, and expected APY. The calculator returns the required monthly contribution.

- How long will it take? Enter the monthly contribution you can afford and the target amount. The calculator returns the number of months to reach the goal and the breakdown of contributions vs. interest earned.

All calculations are done locally in your browser — no account required, no data sent to any server. Your financial information stays private.

Where to Park the Money: Account Types Compared

The right account depends on how soon you'll need the money and how much volatility you can tolerate while you wait. Mismatched accounts are a quiet but expensive mistake — a five-year goal in a checking account loses real value to inflation, while a one-year goal in equities can be devastated by a market drop the month before you withdraw.

0–1 year horizon. Use a high-yield savings account or a money market fund. The headline APY varies widely — online banks frequently offer 3–5x what large incumbent banks pay on basic savings — and the difference compounds even over short horizons. FDIC insurance covers up to $250,000 per depositor per bank. The principal is guaranteed; the only risk is the rate dropping if central bank rates fall.

1–3 year horizon. Consider Treasury bills, brokered CDs, or a CD ladder. Treasury bills are exempt from state and local income tax in the US, which can meaningfully boost the after-tax yield in high-tax states. A CD ladder — staggered maturities at 3, 6, 9, and 12 months — lets you capture longer-duration yields while keeping a portion of the savings accessible without penalty.

3–7 year horizon. The trade-off becomes harder. Pure cash instruments lose meaningful purchasing power over five-plus years; pure equity exposure carries genuine drawdown risk that compounds with the timing of when you need the money. A balanced approach — 60–70% in short-duration bond funds and 30–40% in a broad equity index — splits the difference reasonably well for most savers without requiring active management.

7+ year horizon. A diversified equity index portfolio (low-cost broad-market index funds) historically outperforms cash and bonds over any seven-year period, though with significant interim volatility. For retirement specifically, tax-advantaged accounts (401(k), IRA, Roth IRA, HSA where applicable) almost always beat taxable equivalents, even with their contribution limits and withdrawal restrictions — the tax drag on a taxable account compounds against you decade after decade.

How Behavioral Triggers Boost the Plan's Stickiness

The savings rate that actually shows up in the account at year-end is often 20–40% lower than the rate that was planned in January. The gap isn't usually about income or expenses — it's about how the plan interacts with how humans actually behave. Three structural choices reliably narrow that gap without requiring more discipline or income.

Pre-commit future raises. Decide today, in writing, that the next raise will be split 50/50 between increased savings and lifestyle. Doing it before the raise lands works because the money hasn't yet entered the spending baseline. Doing it after the raise lands almost never works because lifestyle absorbs the increase within a billing cycle. The same logic applies to tax refunds, bonuses, and side income — these are easier to direct to savings if a default destination is set up before the money arrives.

Name the account after the goal. Behavioral economists call this mental accounting, and field studies repeatedly show it matters. A generic "Savings" account leaks more than a "House Down Payment 2028" account, because withdrawing from the named account feels like undermining a specific commitment rather than rebalancing a fungible pool. Most online banks let you create multiple sub-accounts under one login at zero cost — use that capability.

Create asymmetric friction between accounts. Keep the savings account at a different bank than the checking account. The 1–2 day transfer delay disrupts impulsive withdrawals while leaving deposits unaffected. This single change has been shown to reduce "discretionary" withdrawals by a meaningful margin in account-level studies, and it costs nothing.

None of these triggers raise the rate of return on the savings; they raise the rate of contribution. Over a 5–10 year horizon, the rate that gets contributed compounds far more than the rate that gets earned. A 4.5% APY versus a 5.0% APY on $300/month over five years is a difference of about $250. A consistent $300/month versus an inconsistent $230/month average over the same horizon is a difference of about $4,400. The behavioral architecture of the plan, in short, dominates the financial architecture by an order of magnitude.