Inflation is the sustained rise in the general price level of goods and services over time. Its inverse — purchasing power — describes how much a unit of currency can actually buy. Understanding the relationship between inflation and purchasing power is essential for evaluating salary increases, retirement planning, investment returns, and the real cost of long-term savings goals. This guide explains the mechanics of inflation measurement, the math of purchasing power erosion, and how to use the CPI-based inflation calculator to make these abstractions concrete.

What Is Inflation and How Is It Measured?

Inflation is measured by tracking price changes in a representative "basket" of goods and services. In the United States, this is done through the Consumer Price Index (CPI), published monthly by the Bureau of Labor Statistics (BLS). The CPI basket covers about 80,000 items across eight major categories: food, housing, apparel, transportation, medical care, recreation, education, and other goods and services. Housing (primarily "owners' equivalent rent") has the largest weight at around 32% of the index.

The UK measures inflation through the Consumer Prices Index (CPI) and Retail Prices Index (RPI), with the CPI being the official target measure for the Bank of England. The EU uses the Harmonized Index of Consumer Prices (HICP), which allows cross-country comparison. Canada uses the Consumer Price Index published by Statistics Canada; Australia uses the Consumer Price Index published by the Australian Bureau of Statistics.

The Inflation Calculator supports historical CPI data for the US (1980–present), UK, EU, Canada, and Australia, allowing you to calculate the real equivalent of any dollar (or pound, euro, CAD, AUD) amount across any time span covered by the data.

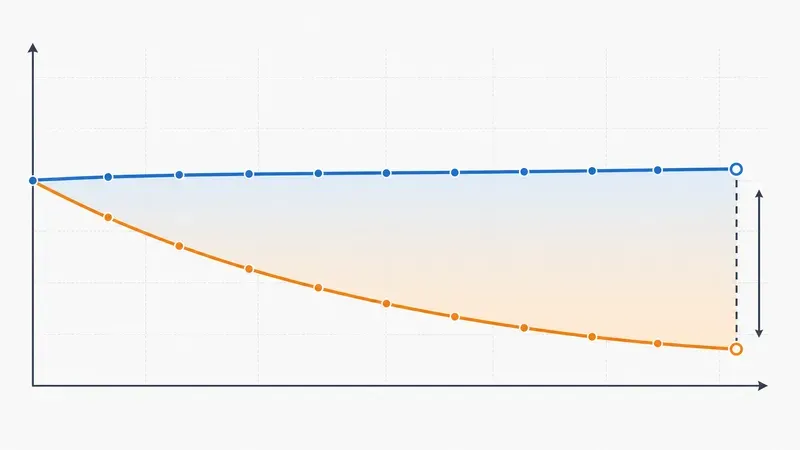

The Math of Purchasing Power Erosion

If the CPI increases from 100 to 130 over a 10-year period, it takes $130 to buy what $100 bought at the start. The purchasing power of the original $100 has declined to $100/1.30 = $76.92 in real terms. Stated differently, $100 lost approximately 23% of its real purchasing power over the decade.

The compound effect of even moderate inflation over long periods is dramatic:

- At 2% annual inflation: $100 in year 0 ≈ $67.30 in real value after 20 years

- At 3% annual inflation: $100 in year 0 ≈ $55.37 in real value after 20 years

- At 4% annual inflation: $100 in year 0 ≈ $45.64 in real value after 20 years

- At 7% annual inflation: $100 in year 0 ≈ $25.84 in real value after 20 years

These figures illustrate why "keeping money in cash" is not risk-free — it carries inflation risk. A savings account earning 0.5% APY when inflation runs at 3% is delivering a real return of approximately −2.5% per year.

Historical Inflation in Context

Understanding the historical range of inflation rates helps calibrate expectations for planning purposes:

- US: The high-inflation era of 1979–1981 saw CPI increases of 11–13% annually. The 1990s–2010s were a period of low inflation, mostly 2–3%. The 2021–2023 episode saw inflation peak at 9.1% (June 2022) before declining back toward the Fed's 2% target.

- EU: The Eurozone generally experienced lower inflation than the US through the 2000s–2010s, often near or below 2%. The 2022 energy crisis drove EU inflation above 10% briefly.

- UK: The UK experienced double-digit inflation in the 1970s and early 1980s. The inflation targeting era (post-1992) kept it near 2%. The 2022–2023 episode pushed UK CPI above 11%.

For long-term financial projections, most financial planners use 2.5–3% as a conservative base case for developed economy inflation, with scenario testing at 4–5% for stress testing.

Nominal vs. Real Returns: Why the Distinction Matters

A nominal return is the headline percentage increase in a money value. A real return is the inflation-adjusted return — what the investment actually earned in purchasing power terms. The approximate relationship (Fisher equation) is:

Real Return ≈ Nominal Return − Inflation Rate

More precisely: Real Return = (1 + Nominal Rate) / (1 + Inflation Rate) − 1

Examples:

- A savings account earning 1.5% nominal when inflation is 3.5% has a real return of approximately −2.0%

- A bond yielding 4.5% nominal when inflation is 2.5% has a real return of approximately +2.0%

- A stock portfolio returning 10% nominal when inflation is 3% has a real return of approximately +7.0%

Evaluating any investment, salary offer, or savings rate without adjusting for inflation risks making decisions based on money illusion — confusing a nominal increase with a real one.

Practical Uses of an Inflation Calculator

The Inflation Calculator serves several common financial planning purposes:

- Historical salary comparison: "I made $45,000 in 2005 and I'm being offered $65,000 now — am I ahead in real terms?" (CPI shows $45,000 in 2005 ≈ $71,000 in 2024 dollars — so the $65,000 offer is actually below the 2005 real wage)

- Retirement income planning: "I want $4,000/month in today's dollars when I retire in 25 years at 3% inflation — how much will that require in nominal dollars?" (approximately $8,375/month)

- Savings goal adjustment: "My savings goal is $50,000 for a house down payment in 5 years — what will prices be if inflation averages 3%?" (approximately $57,964)

- Historical cost curiosity: "What would $1,000 from 1990 buy in today's prices?" (about $2,500 in 2024 US dollars)

- International comparison: How have CPI rates differed across major economies over the same time period?

Inflation and Retirement Planning

Inflation poses the greatest risk for retirees — people who have exited the labor market and can no longer respond to rising prices with higher earned income. A retiree who budgets for $5,000/month in today's dollars but does not adjust for inflation will find their fixed income covering progressively less over a 20–30 year retirement. At 3% annual inflation, their purchasing power halves in approximately 24 years.

Strategies that address inflation risk in retirement:

- Social Security COLA: Social Security benefits are adjusted annually for inflation via the Cost of Living Adjustment (COLA), providing a base level of inflation protection

- TIPS (Treasury Inflation-Protected Securities): US government bonds whose principal adjusts with CPI, providing direct inflation hedging

- Equity allocation: Stocks have historically outpaced inflation over long periods, though with significant volatility

- Inflation-indexed annuities: Provide guaranteed income that rises with CPI, at the cost of a lower initial payout

- Rental real estate: Rents generally track inflation over time, making rental income a natural inflation hedge

For retirement planning specifically, see how savings interact with inflation using the Savings Goal Calculator — enter a projected inflation-adjusted target to understand the contributions needed in today's dollars.

How the Inflation Calculator Works

The calculator offers two modes:

- Historical mode: Uses actual CPI index values for the selected country to compute the precise purchasing power equivalent between two years. This is the most accurate calculation for past-to-past or past-to-present comparisons, because it uses real measured price changes rather than assumed rates.

- Projected mode: Uses a user-specified annual inflation rate to project the equivalent value of a present amount in a future year, using the standard compound future value formula: FV = PV × (1 + r)^n. This mode is useful for planning scenarios where the future is uncertain.

All calculations run entirely in your browser. No data is sent to any server. Financial amounts you enter are private to your session.

Personal Inflation vs Headline CPI: Why They Diverge

The published CPI represents the price change of a basket of goods and services purchased by an average household. Your household is not the average household. If a disproportionate share of your spending goes to categories with above-average inflation — healthcare, education, urban housing, eldercare — your personal inflation rate can run 1–3 percentage points above the headline figure, year after year. That gap compounds: a personal inflation rate of 5% versus a headline of 3% over ten years means roughly 22% more cumulative purchasing-power loss than the published number would suggest.

Three categories drive most of the divergence. Healthcare historically inflates 1–2 percentage points faster than headline CPI in the US, and the gap widens with age as the share of healthcare in personal spending grows from roughly 6–8% in middle age to 15%+ in retirement. Higher education tuition has run 2–4 percentage points above headline CPI for decades; for households with college-bound children, this category alone can move the personal inflation rate noticeably. Urban housing, both rent and ownership costs, has substantially exceeded national average shelter inflation in major metropolitan areas for the last 15+ years — households in those metros experience a different inflation reality than the national average.

Conversely, some categories deflate or barely inflate — consumer electronics, telecommunications, and some categories of clothing. Households whose spending skews toward these categories may experience inflation below headline. The practical takeaway: when planning for retirement, healthcare costs, or education, don't assume the headline CPI captures your personal trajectory. Build a personal estimate by weighting category inflation rates against your actual spending, and use that figure in the calculator's projection mode rather than the published national average.

Inflation Hedges: What Actually Preserves Purchasing Power

If inflation erodes the real value of cash and fixed-income assets, what reliably preserves purchasing power over multi-decade horizons? The historical record points to a small number of asset categories, each with trade-offs.

Inflation-protected government bonds (TIPS in the US, index-linked gilts in the UK, equivalent instruments elsewhere) explicitly adjust principal with the published CPI, providing a near-direct hedge. The trade-off is yield: real yields on TIPS have ranged from negative to modestly positive in the last 20 years, so they preserve purchasing power but don't grow it meaningfully. They're a defensive instrument, not a growth one.

Broad equity ownership has historically outpaced inflation over rolling 15–20 year periods, though with significant interim drawdowns and meaningful sensitivity to the inflation regime. Companies with pricing power — the ability to pass cost increases through to customers without losing volume — perform especially well in moderate inflation. The 1970s saw extended periods of negative real equity returns, however, so the hedge isn't universal across all inflation environments.

Real assets — owner-occupied housing, productive land, and to a lesser extent commodities — tend to preserve purchasing power because their replacement cost rises with general prices. Owner-occupied housing additionally provides an implicit return through avoided rent inflation, which is meaningful in metros where rents rise faster than headline CPI. Commodities are volatile and don't produce cash flow, so they're a tactical hedge rather than a portfolio cornerstone.